Having detailed records aids in spotting errors or unusual cost patterns early on. Regular reviews can flag issues before they grow into bigger problems. A well-documented trail of COGS makes auditing simpler and more transparent too, reducing risks of financial mishaps. Moving onto “The Importance of Recording COGS in Journal Entries,” it’s clear why capturing this information accurately matters for any business.

The Impact of COGS on Company’s Net Income

This example illustrates how COGS is determined and the importance of accurate inventory tracking for retail businesses in assessing their cost of sales. This entry matches the ending balance in the inventory account to the costed actual ending inventory, while eliminating the $450,000 balance in the purchases account. Let’s say you have a beginning balance in your Inventory account of $4,000.

Limitations of COGS

In accounting journal entries, debiting COGS reflects an increase in expense as goods are sold, impacting your income statement by reducing net income. If you buy $100 in raw materials to manufacture your product, you would debit your raw materials inventory and credit your accounts payable. Once that $100 of raw material is moved to the work-in-process phase, the work-in-process inventory account is debited and the raw material inventory account is credited. A company’s ability to minimize costs and maximize sales will ultimately determine its gross profit.

Cost of goods sold in a service business

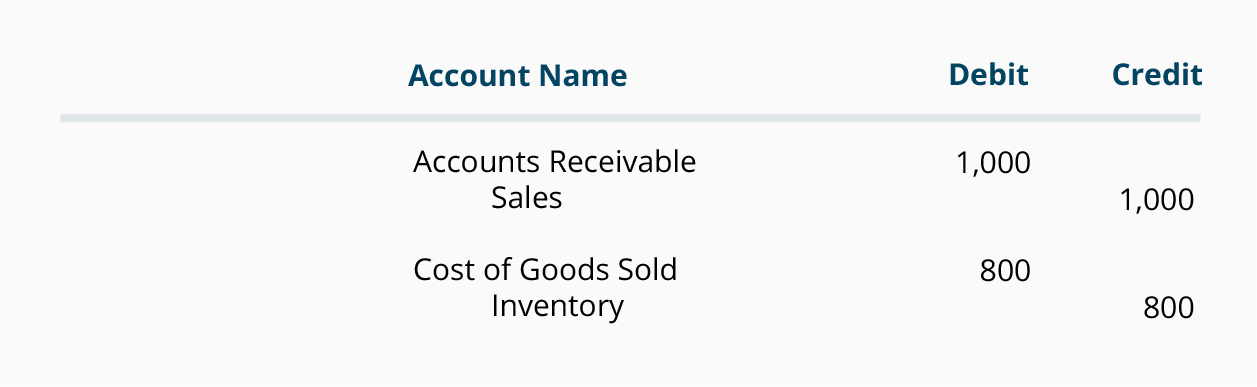

You should record the cost of goods sold as a debit in your accounting journal. Under the periodic inventory system, we usually need to take the physical count of the ending inventory before we can determine and record the cost of goods sold to the income statement. Conversely, you’ll credit your inventory account to decrease the assets on your balance sheet, as the number of goods available for sale drops. The dance between these two accounts, debits in COGS and credits in inventory, is a choreographed reflection of your business’s operations over the period. Your income statement includes your business’s cost of goods sold.

- These inventory items may be commodities or extracted materials that the firm or its subsidiary has produced or extracted.

- It helps you set prices, determine if you need to change suppliers, and identify profit loss margins.

- When calculating COGS, the first step is to determine the beginning cost of inventory and the ending cost of inventory for your reporting period.

- Selling the item creates a profit, but a portion of that profit was lost, due to the cost of making the item.

This decrease shows up in the books as a debit to Cost of Goods Sold and a credit to Inventory. This article will walk through the basics—calculating COGS and making accurate journal entries—to give you clearer insights into where your money goes after every sale. And by demystifying these fundamental steps in accounting practice, we’ll help safeguard against errors creeping into your books. Meanwhile, with Ramp’s accounts payable software, you can eliminate manual data entry, automate payments to vendors and suppliers, and close your books faster than ever. No matter how COGS is recorded, keep regular records on your COGS calculations. The average cost method, or weighted-average method, does not take into consideration price inflation or deflation.

Is cost of goods sold a debit or credit balance?

The equation forinventory turnover is the cost of goods sold (COGS) divided by the average inventory. Inventory turnover is also known as inventory turns, stockturn, stock turns, turns, and stock turnover. Ultimately, having a deep understanding of COGS can help businesses remain competitive and profitable in the long term. Please note the LIFO is not an acceptable costing method in Canada. At the beginning of the year, the beginning inventory is the value of inventory, which is the end of the previous year.

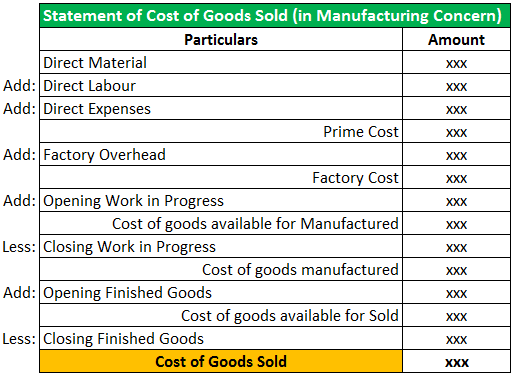

The Cost of Goods Sold (COGS) is an important component of the financial information reported by a business and is used to calculate various metrics such as gross margin and net income. However, recording COGS accurately can be complicated by variables such as shipping delays, returns, and missing vendor invoices – just to name a few. In certain scenarios such as when sales impact multiple periods, recording COGS in the appropriate period can be difficult due to system limitations. We dive deeper into these technology challenges in this blog post. There are other inventory costing factors that may influence your overall COGS. The CRA refers to these methods as “first in, first out” (FIFO), “last in, first out” (LIFO), and average cost.

The average cost method stabilizes the item’s cost from the year. Using FIFO, the jeweler would list COGS as $100, regardless of the price it cost at the end of the production cycle. When tax time rolls around, you can include the cost of purchasing inventory on your tax return, which could reduce your business’ taxable income.

What’s more, coupling products like A2X with QBO creates a duo that automates much of the legwork involved in accounting. This includes purchase invoices, shipping records, and inventory records. Reconcile Inventory with purchases and sales records on a schedule, and correct any discrepancies right away. Welcome to AccountingFounder.com, your go-to source for accounting and financial tips. Our mission is to provide entrepreneurs and small business owners with the knowledge and resources they need.

The COGS typically does not appear directly on the balance sheet. Instead, COGS is reported on the income statement and directly affects the inventory figures which are shown on the balance sheet. The balance sheet reflects the ending inventory, which is directly influenced by the COGS calculation. In these how to record cost of goods sold journal entry cases, the IRS recommends either FIFO or LIFO costing methods. COGS can vary significantly from one period to another due to changes in raw material costs, manufacturing efficiency, and production volume. Such fluctuations make it difficult to predict future financial performance based purely on COGS.

Ensuring that your Cost of Goods Sold (COGS) is recorded accurately is not just about meticulous bookkeeping, but it plays a critical role in the financial health of your business. By tracking spending, analyzing trends, and making strategic decisions, you’re harnessing the power of COGS to inform crucial aspects of your business operations. Debit your COGS account and credit your Inventory account to show your cost of goods sold for the period. Your COGS must match up to revenue in the same accounting period.